Language

Language How to buy a house in France? Requirements & more

Become the new owner of a home with a view of the Eiffel Tower! Find out all the steps involved in buying a house in France.

France is known for its stable property market, and foreigners can buy a home there without being residents. Before buying property, however, it’s important to understand the legal requirements and how the process works.

This guide explains what international buyers need to know before buying property in France, whether you’re buying as an investment, a primary residence, or a holiday home. We’ll cover the legal requirements, taxes, mortgage options, and other important details. You’ll also find an overview of current property prices in different parts of France. If you’re planning to buy property in France in 2026, this guide will help you understand the process and avoid common mistakes.

Requirements for foreigners to buy a house in France

If you’re thinking about buying property in France, you’ll be glad to know that foreigners are welcome to do so. EU and non-EU citizens can buy a home under almost the same conditions as French buyers. However, there are a few legal and financial requirements to understand before you begin.

1. Types of properties

Most properties in France are sold with full ownership, meaning you own both the property and the land. However, there are also a few less common ownership options, such as:

- Co-ownership (copropriété): You buy a home in a residential building or complex and share maintenance costs with the other property owners.

- Through a real estate company (SCI, Société Civile Immobilière): The property is held in the company’s name, and you own shares in the company.

- Usufruct or bare ownership: You are the legal owner of the property, but you cannot use it until the usufruct ends due to death or the expiration of the term.

2. Residency and visa requirements

Buying a home in France does not automatically give you residency, and you don’t need to be a resident to buy property. If you’re an EU citizen, you can live in France without a visa. If you’re from outside the EU and want to stay for more than 90 days, you’ll need a residence visa. If you’re moving to France for work, study, or as a digital nomad, you’ll need to apply for the right visa before you move.

3. Legal limits and real estate restrictions

Foreigners can buy most types of property in France without any restrictions. The main exceptions are some rural land, properties in protected or historic areas, and certain homes used for short-term rentals in Paris. In general, you can buy apartments, houses, villas, building plots, and commercial properties without any problems.

4. Required documents

To buy property in France, you’ll usually need a valid passport, proof of income, recent bank statements, your latest tax return, and documents showing where the funds for the purchase come from.

5. Financial requirements

If you need a mortgage, French banks can lend to foreign buyers. They’ll check your financial history, income, debts, and savings to make sure you can afford the loan. In most cases, they’ll lend up to 70%–80% of the property’s value.

How much does a house cost in France?

Property prices in France vary depending on the city, location, and type of home. In general, homes are more expensive in major cities like Paris and in coastal areas, while prices are lower in many inland regions. Here’s a comparison of average prices in different parts of the country:

- Paris → $11,400 (€9,690) per m²

- Nice → $6,100 (€5,200) per m²

- Lyon → $5,300 (€4,500) per m²

- Marseille → $4,160 (€3,530) per m²

- Nantes → $4,070 (€3,455) per m²

- Montpellier → $3,910 (€3,325) per m²

- Lille → $3,950 (€3,360) per m²

- Le Mans → $2,320 (€1,970) per m²

- Limoges → $1,845 (€1,565) per m²

The national average is around $2,590 (€2,200) per m². Property prices depend on factors such as the location, access to public transport, nearby schools, hospitals and shops, the condition of the property, and whether the area is popular with tourists.

With the average monthly salary in France at around $2,800 (€2,380), many buyers look beyond Paris to smaller cities where property is more affordable. For example, a 50 m² apartment in central Paris costs around $570,000 (€484,500), a 90 m² house in Lyon about $450,000 (€382,500), a 100 m² home in Toulouse around $320,000 (€272,000), and a rural property inland about $180,000 (€153,000). You should also budget around 1% to 3% of the home’s value each year for maintenance.

Property taxes in France

Buying and owning a home in France involves several upfront costs and taxes over time. The French tax system also treats residents and non-residents differently, which can affect your overall tax liability. When buying a property in France, you will need to pay the following initial costs:

| Tax | Approximate cost |

| Real Estate VAT (TVA) | About 20% for new homes only |

| Registration and notary | 7–8% |

| Appraisal | $300–900 for standard homes |

| Mortgage closing costs | Between 0.5% and 1% of the loan amount |

| Mortgage interest | Between 3% and 4.5% per year |

| Example: A home priced at $300,000 | Between $21,000 and $24,000 |

After buying a property, you will need to pay annual property taxes of around $1,200–3,000 (€1,020–2,550), depending on the home’s value, plus community fees of around $1,200–3,500 (€1,020–2,975) per year. If you sell the property later, you may need to pay about 19% tax on your profit, plus 17.2% in social charges. For example, a profit of $80,000 (€68,000) could result in around $28,960 (€24,480) in taxes.

On the other hand, there may be tax benefits if the property is your main home. France also has double taxation agreements with countries such as Spain, Germany, Italy, the Netherlands, and Portugal, so you won’t have to pay tax twice on the same income or asset.

Steps to buying a house in France

Buying a house in France is a structured and safe process involving real estate agents, banks, and notaries. To help you understand the steps and avoid mistakes, here is what you need to know.

1. Searching for properties: Websites and real estate agencies

The first step is finding the right property. You can start by browsing property websites such as SeLoger, Properstar, and Leboncoin. If you are already in France, you can also visit a local real estate agency for help. Most property sales in France are handled through estate agencies, particularly in larger cities such as Paris and Lyon. This process usually takes between one and three months.

2. Legal verification of the property

Once you find a home, it’s important to check its legal status before making an offer. Ask your notary to check the ownership, any outstanding debts, building rules, and other legal details. In France, the notary handles this process, and you can usually get this information within a few days.

3. Negotiation and initial offer

Once you’re satisfied with the property’s condition and legal status, it’s time to make a formal offer. In France, you can negotiate the price of resale properties, but there is usually limited room for negotiation. The seller will normally respond within about a week.

4. Reservation and financing

Once the price has been agreed, you’ll usually sign a preliminary sales agreement and pay a deposit of around 5% to 10% of the purchase price. After signing the sales agreement, you can arrange a mortgage if needed or complete the purchase with the notary within one to two months. You also have 10 days by law to cancel the purchase and get your money back if you change your mind.

5. Signing of the deed and registration

This is the final stage of the purchase. You will sign the contract with the notary, pay the remaining amount, and officially become the owner. After the deed is signed, the notary registers the sale with the French land registry. You’ll receive proof of ownership shortly afterwards.

How do you pay for a house in France?

The usual way to pay for a home in France is by bank transfer to the notary, not the seller. The notary holds the money and makes sure the payment is secure until the purchase is completed. You can transfer the money from your own country’s bank or from a French bank.

f you need a mortgage, French banks usually cover 70% to 80% of the property’s value. Foreign buyers may need to meet extra requirements, such as a 20% to 30% down payment, life and home insurance, and proof of income. Interest rates are usually between 3% and 4%, and can be higher than 4.5% for riskier applicants. Other options include:

- Cash payment: The simplest option, with no interest.

- Private financing: Loans from individuals or investors.

- Mortgage in your home country: You can apply for a mortgage at your bank, where they already know your credit history, and it may be more advantageous.

Keep in mind that international transfer fees and exchange rate changes can affect the final price. For example, a 2% exchange rate difference on a $300,000 (€255,000) property could cost you more than $6,000 (€5,100).

Tips before buying a house in France

As this guide has shown, buying a home in France is a straightforward process, but it’s important to pay attention to the legal and financial details. With the right preparation and these practical tips, you can make the purchase with confidence and avoid common issues.

Make sure you have a good internet connection

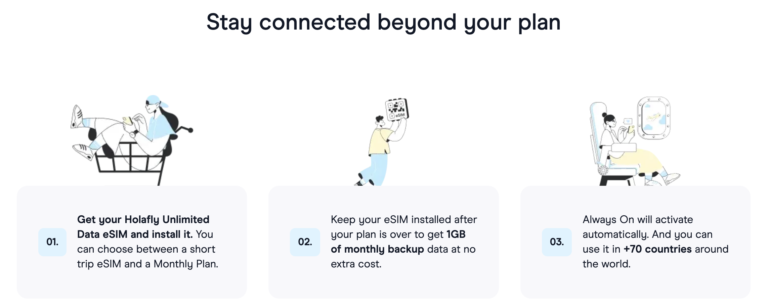

First, get a reliable internet connection so you can search for homes online, make secure payments, and travel between France and your home country without changing eSIMs. We recommend Holafly’s monthly plans, which include 25 GB or unlimited data and let you connect multiple devices at the same time. With the Always On benefit, you also get 1 GB of free data for life if you cancel your plan or need it in an emergency.

Get 1GB of monthly backup data, no extra cost

If you only need internet for a few days, you can choose Holafly’s France eSIM, which gives you unlimited data only for the days you need, starting at $3.90 per day. Now that you know how to stay connected in France, here are some final tips to help you with the process.

Tips for buying a home in France safely

- Review all legal documents: Before signing any contract, verify the ownership and ensure there are no liens or debts.

- Seek local advice: Seek advice from local experts, such as a real estate agent or property lawyer. They can help with the paperwork and translation if needed.

- Carefully evaluate the area: In addition to the house itself, consider its surroundings, including transportation options, amenities, safety, and future urban development projects.

- Assess the market before buying: Compare prices per square meter in the area and research rental demand, if you’re investing.

- Be aware of legal risks for foreigners: Find out about tax differences for non-residents and local regulations regarding short-term rentals.

- Rent before you buy: Renting first gives you time to explore the area, get a feel for the neighborhood, and decide whether it suits your lifestyle.

- Watch out for common signs of fraud: Although scams are not common in France, you should watch out for warning signs such as unusually low prices, pressure to make quick payments to personal accounts, or suspicious changes to bank details.

Frequently asked questions about buying a house in France

Yes. Foreigners can buy property in France without being residents. However, if you are not an EU citizen and want to stay in France for more than 90 days, you will need to apply for a visa.

French banks usually require a down payment of 20% to 30%. You should also budget for upfront costs, such as the property valuation, registration fees, and notary fees.

The entire process of buying a house in France can take between three and six months, from the time you find the property until the signing at the notary’s office.

Yes, a notary is required for all real estate sales to ensure the transaction is legally valid.

Yes, but it depends on local regulations. For example, Paris has certain restrictions on short-term rentals that you should be aware of beforehand.

In France, you have a 10-day cooling-off period after signing the sales agreement. If you change your mind, you can cancel the purchase and get your deposit back.

Plans that may interest you

Hi! I'm a Spanish-English translator working with Holafly, helping bring travel content to life for curious travelers. As a digital nomad with a passion for exploring, I'm always adding new spots to my bucket list. If you love to travel like me, stick around because you're in the right place to find inspiration for your next trip! ✈️🌍