Language

Language Buy a house in the Philippines as a foreigner: Comprehensive guide

Find out how to buy a house in the Philippines! We'll explain the legal regulations for foreigners, the requirements, and current prices.

If you’re thinking about buying a house in the Philippines as an investment or a holiday home, make sure you understand the local property rules first. Foreign buyers are allowed to purchase property, but there are limits, particularly when it comes to owning land.

In this guide, we’ll walk you through the key things to know before buying property in the Philippines. We’ll cover the legal requirements, necessary documents, available property types, and what the current Philippine real estate market looks like. We’ll also cover the taxes you may have to pay and take you through the buying process, from finding the right property to completing the purchase.

Requirements for foreigners to buy a house in the Philippines

Before you buy property in the Philippines, make sure you’re familiar with the rules that apply to foreign buyers. Although land ownership is restricted, foreigners can still invest in certain types of property.

1. Types of property available to foreigners

Foreigners are allowed to buy condominium units in the Philippines. This means you can own your individual unit while sharing ownership of common areas such as hallways, elevators, gardens, and other facilities with other residents. However, no more than 40% of the units in a condominium development can be owned by foreigners, with at least 60% reserved for Filipino owners.

If you’re looking to buy a house with land, it’s important to know that only Filipino citizens can legally own land. As a foreigner, you can lease the land for up to 50 years, with the option to extend the lease for another 25 years. This means you’ll own the house, but not the land.

2. Required documentation

You don’t need to be a Philippine resident to buy property, but having residency status may make some parts of the process easier, especially when dealing with banks. If you plan to live in the Philippines, work remotely, or stay for a longer period, you’ll need to apply for the right visa. Keep in mind that buying a home in the Philippines doesn’t give you the right to live there; you’ll still need a valid visa or residence permit.

To buy property in the Philippines, you’ll typically need your passport, a sale and purchase agreement, the property title, proof of registration, and evidence that you have sufficient funds to complete the purchase.

3. Basic financial requirements

Getting a mortgage in the Philippines can be difficult for foreign buyers, so many choose to pay from their own savings. Before buying, make sure you have enough money for the deposit and a plan to cover the rest of the purchase price, whether that’s with cash or financing from a local or international lender.

4. Hire a lawyer or notary

Buying property in the Philippines as a foreigner is much easier with professional advice. A lawyer or real estate expert can check the contract, explain any legal terms, and make sure the purchase follows local laws. Once all documents are prepared, a notary public will oversee the official signing and completion of the sale.

5. Purchase through a company or with a Filipino partner

If you’re married to a Filipino citizen and plan to purchase land together, the land must be registered in your Filipino spouse’s name. You can use the property, but you can’t own the land. You can also buy through a company, as long as at least 60% of it is owned by Filipino citizens. This option is usually only used for large investments.

How much does a house cost in the Philippines?

Buying a house in the Philippines is generally cheaper than in many European countries. Prices vary depending on the city, the neighborhood, and the type of property. Things like nearby transport and local amenities can also affect the price. Here are the average prices per square metre in some of the country’s main cities:

- Central Manila: $2,000–3,500 per square meter

- Manila (suburbs): $1,000–2,000 per square meter

- Cebu: $1,200–2,500 per square meter

- Davao: $800–1,500 per square meter

- Rural areas: $300–800 per square meter

The most expensive properties are in Metro Manila, especially in business districts like Makati and Bonifacio Global City. A 60 m² condo there typically costs between $120,000 and $210,000. In cities like Cebu, an 80 m² apartment usually costs between $80,000 and $160,000. If you’re looking in smaller towns or rural areas, where there are fewer services and less infrastructure, you can find houses starting at around $30,000.

The average monthly salary in the Philippines is around $300–600, so buying a home in the country’s main cities is too expensive for many local people. Many of these properties are bought by foreign investors instead. Besides the purchase price, you’ll also need to budget for the following annual costs:

- Condominium fees: $600–2,000

- General maintenance: $300–1,000

- Utilities (water, electricity): $600–1,500

Taxes on a house in the Philippines

Besides the cost of the property itself, you’ll also need to pay a number of taxes and fees. Some apply when you buy the home, others while you own it, and some if you decide to sell it later. Here’s a summary of the main costs you’ll face when buying property in the Philippines.

| Tax | Approximate Cost |

| Transfer Tax | 0.5–0.75% of the value |

| Registration and Notary Fees | 0.75–1.5% |

| Document Stamp Tax | About 1.5% |

| Appraisal, if you apply for a mortgage | $100–300 |

| Origination fee | 0.5–1% |

| Mortgage interest | Between 5% and 8% per year |

| Example: A home worth $100,000 | Between $3,400–5,350 |

Once you own the property, you’ll need to pay some yearly taxes and local fees. These include the Real Property Tax (RPT), which is usually 1% to 2% of the property’s assessed value, and, in some areas, a local community tax. For example, if your home is worth $100,000, the RPT could be around $200–600 a year. If you sell the property later, you’ll also pay a 6% tax based on whichever is higher: the sale price or the property’s assessed value.

Property taxes in the Philippines are the same for residents and non-residents. However, tax rates can vary by location, with smaller towns often charging less. It’s also a good idea to check if your home country has a double tax treaty with the Philippines. If it does, you may not have to pay tax twice on the same income or gain.

Steps to buying a house in the Philippines

Buying a home in the Philippines usually takes 6 to 12 weeks. To help you through the process, we’ve outlined the main steps below. Take your time with each one, especially when checking the property’s legal status, to avoid scams or other problems.

1. Search for properties (1–4 weeks)

The first step is to find a property that suits your budget. You can search on websites like Lamudi Philippines, Dot Property, and PropertyMart, or contact a local real estate agency. Make sure the agency is licensed and registered. If you’re buying from overseas, ask for a live video tour so you can see the property before making a decision.

2. Verify the property’s legal status (1–2 weeks)

The next step is to confirm that the property is legally registered and that the seller has the right to sell it. Don’t rely only on the seller’s information. Ask for the property title, registration documents, proof of ownership, and confirmation that there are no unpaid debts or legal problems. If it’s a condo, make sure the building follows the 40% limit for foreign owners.

3. Negotiate the price and terms (1 week)

In the Philippines, negotiating the price of a resale property is common. Make an offer through the real estate agent and agree on the final price with the seller. You should also confirm the payment terms, timeline, and what is included in the sale, such as furniture, parking, or appliances.

4. Sign the preliminary contract and pay the deposit (1 week)

Once you agree on the price, you can reserve the property with a preliminary contract. You will usually need to pay a 1% to 5% deposit to show your commitment to buying it. This usually keeps the property off the market while the final paperwork and checks are completed.

5. Complete legal review (2–4 weeks)

Before moving forward, have a lawyer review everything related to the property. They should confirm that the documents are valid, the property is properly registered, taxes are up to date, and the purchase follows the rules for foreigners. Doing this early can help you avoid legal issues in the future.

6. Final signing and registration (1–2 weeks)

After the legal checks are complete, you can arrange the final signing with the notary. You will make the final payment, receive the keys, and the property title will be transferred to your name in the Land Registry. At this point, the property officially belongs to you.

How do you pay for a house in the Philippines?

Most people pay for property in the Philippines by bank transfer, either from their own country or through a local bank account. Opening a local account may require a visa or residency, but it can make payments easier and reduce fees.

Many foreign buyers choose to pay without local financing, either using their own money or an international personal loan. Banks also carry out checks to comply with anti-money-laundering regulations, so you may need to provide documents showing the source of your funds. Also, exchange rates can affect the final cost by several thousand dollars or euros.

If you don’t want a mortgage but cannot pay the full amount upfront, some sellers may offer payment plans directly to buyers. However, this should be done carefully, with proper legal advice and a notarized agreement.

Tips before buying a house in the Philippines

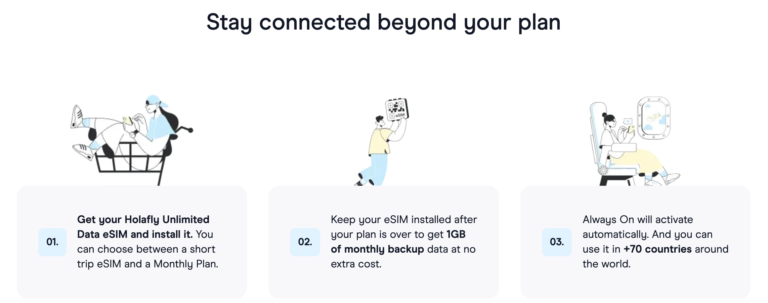

Having a reliable internet connection before, during, and after the purchase process is essential. It allows you to handle paperwork, stay in touch with your real estate agent, join video calls, and check documents online. For foreign buyers, Holafly offers practical solutions to help you stay connected.

If you only need internet for a few days, Holafly’s Philippines eSIM is a simple option, with unlimited data from $3.90 per day. If you plan to stay longer, you can choose one of Holafly’s monthly plans with 25 GB or unlimited data. The same eSIM can be used in more than 160 destinations. Plus, if you cancel your subscription, Always On gives you 1 GB of free data forever in over 70 countries, so you can stay connected.

Tips for a safe purchase

- Review all the documentation: Do not sign anything before verifying that the property is legally valid, free of liens, and registered.

- Hire a local legal advisor: The safest way to buy a home in the Philippines is to work with a real estate agency or a lawyer who can help check the documents and contracts.

- Research the area before buying: Check whether the area has good transport links, nearby services, hospitals, schools, and is generally safe. These factors will affect both your quality of life and the property’s future value.

- Research the market before making a decision: Compare prices by neighborhood and property type so you’ll know how much you can negotiate and avoid overpaying.

- Keep in mind the legal restrictions for foreigners: If you buy a condo, at least 60% of the units must be owned by local buyers, with a maximum of 40% available to foreigners.

- Identify common signs of fraud: Prices well below market value, lack of documentation, and a rush to close the deal.

- Rent before you buy: If you plan to live in the Philippines, consider renting in the area for a few weeks first. This will help you see if you like the location and make a better decision before buying.

Frequently asked questions about buying a house in the Philippines

It’s not required, but it can make the process easier. In most cases, you can buy property with just your passport, even if you are not a resident.

If you want to buy a home in the Philippines, you cannot own the land it sits on as a foreigner, but you can have the right to use it. However, you can fully own a condo unit as long as at least 60% of the owners in the building are Filipino citizens.

Getting a mortgage in the Philippines can be difficult if you are not a resident. Interest rates are also quite high, so you may want to look into financing options in your home country or arrange a payment plan directly with the seller.

Yes, many foreigners buy property in the Philippines as an investment and rent it out, especially in places like Manila and Cebu. Just make sure to check the local rental rules in the area before you do so.

You should factor in an additional 3% to 5% for taxes, closing costs, and potential mortgage costs.

Plans that may interest you

Hi! I'm a Spanish-English translator working with Holafly, helping bring travel content to life for curious travelers. As a digital nomad with a passion for exploring, I'm always adding new spots to my bucket list. If you love to travel like me, stick around because you're in the right place to find inspiration for your next trip! ✈️🌍